The structure is below, followed by worked examples, the retention test, the tax position, and the answers to the questions sellers usually raise.

The structure, in one paragraph

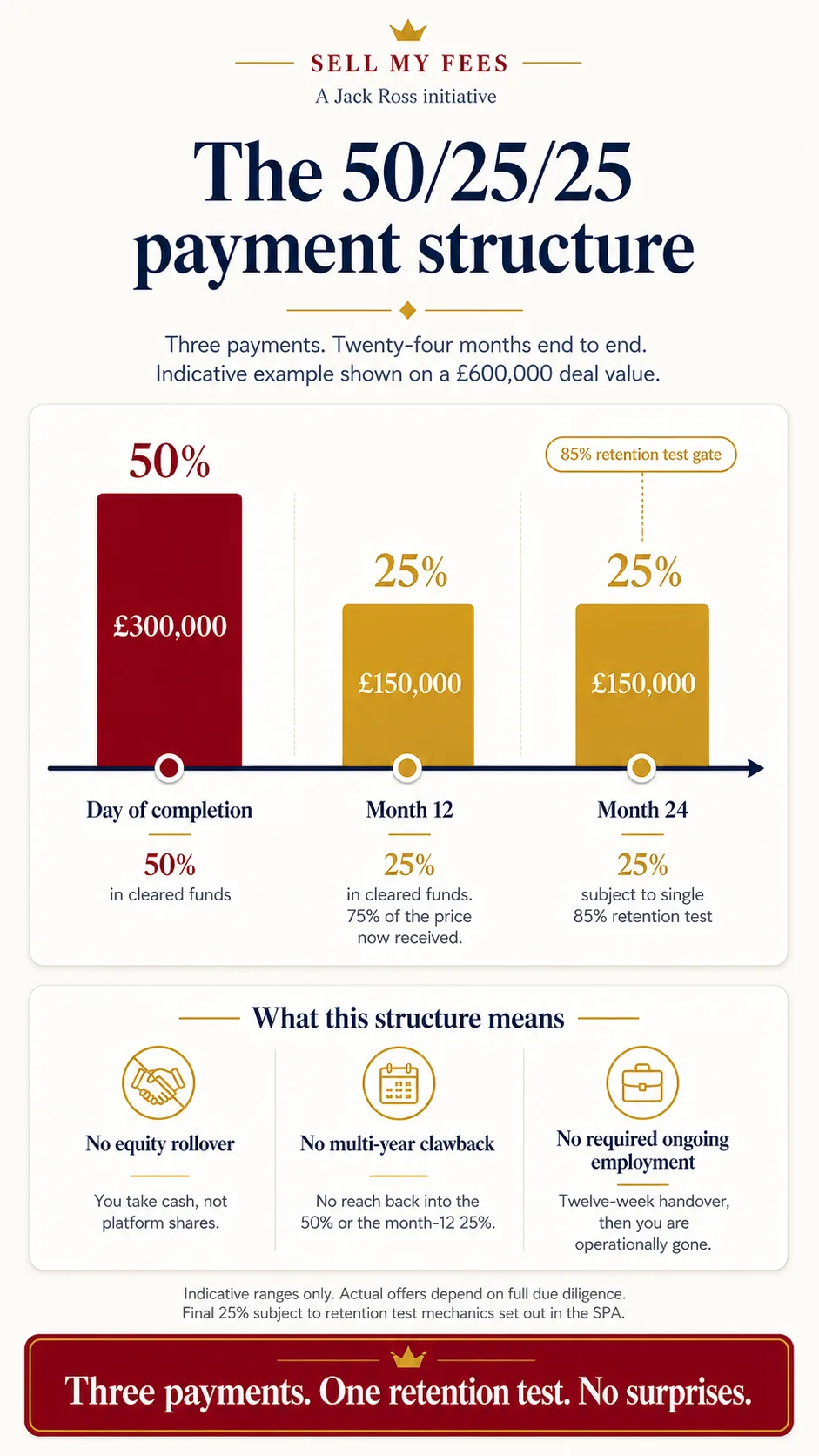

50 per cent on completion, in cleared funds. 25 per cent at month 12, in cleared funds, so three-quarters of the price is in your account within a year. 25 per cent at month 24, subject only to a single retention test. Gross recurring fees from the acquired client base must be at least 85 per cent of completion-date recurring fees, adjusted for natural attrition. No clawback against the first two payments. No equity rollover required. No earn-back through performance metrics. No required continuing employment. No broker fee. The commercial structure is simple enough to summarise in the paragraph you have just read. The legal SPA itself runs to thirty to fifty pages and is reviewed by both solicitors.

How the 85 per cent retention test works

One number, one moment, one calculation. The figures below are illustrative but the mechanics are the actual mechanics.

Retention above the threshold (full payment). Completion-date recurring fees from the acquired client base: £350,000. Month-24 recurring fees from the same client base: £310,000. Retention is 88.6 per cent. The full final 25 per cent is paid because retention is above 85 per cent.

Retention below the threshold (sliding scale). Same starting position. Month-24 recurring fees: £285,000. Retention is 81.4 per cent. The final payment is reduced under the sliding-scale formula in the SPA. The exact formula is shared and agreed before heads of terms are signed. It is not a buyer-side surprise.

Adjustments for natural attrition. The denominator is adjusted for clients lost through circumstances unrelated to the deal. These include client deaths, client retirements, client business closures unrelated to the change of accountant, and any clients we mutually agree to off-board at completion. The adjustments are agreed at heads of terms and written into the SPA.

What could reduce the final 25 per cent

- Voluntary client loss below the 85 per cent threshold. Clients who choose to leave following the change of accountant, beyond the natural attrition allowance, count against the test. The threshold is set well above what a careful introduction normally delivers.

- Seller continuing professional involvement with acquired clients. If you take on continuing professional work for a client whose fees are in the acquired book, those fees are removed from the month-24 numerator. We agree explicit carve-outs at heads of terms for any clients you intend to retain.

- Mutually agreed off-boards. Any client we agree at completion to part company with does not count for or against. The list is in the disclosure letter.

- Buyer-caused attrition. If a client leaves citing the buyer's conduct (a fee hike, a software switch, a relationship breakdown with the new partner), the SPA sets out a dispute mechanism. The default position is that buyer-caused losses are excluded from the test. A short escalation route is written into the document so the test does not turn into a litigation point.

How a PE consolidator typically structures the same deal

For comparison, the structure widely observed at the larger PE-backed UK platforms looks broadly like this (the specifics vary by platform and by deal):

- 30 to 60 per cent cash on completion (sometimes lower at the small end of the platform's range)

- Equity rollover of 20 to 40 per cent of consideration into platform shares, locked up until exit

- Earn-out of the residual cash component over 36 to 60 months, conditional on multiple performance metrics

- Clawback if performance metrics are missed in any of the earn-out years, often retroactive across the period

- Continued personal involvement of the seller through the earn-out period as a condition of full payment

The headline multiple is higher in this model. The cash-out structure is significantly slower. The economic risk to the seller persists for years. The seller is, in a real sense, an unsecured creditor of the platform for the back-end of their consideration.

Both models work for different sellers. If you want the highest possible headline number and you are willing to remain economically tied to the buyer for five years, a PE platform may be the right answer for you. If you want a clean structure with most of your money in your hands within 24 months and no continuing economic exposure, our structure is built for that.

GRF multiples: what we pay

The realistic UK general-practice range in 2026 is:

- 0.8x to 1.0x GRF. Books with one or more risk factors: low recurring proportion (under 50 per cent), heavy concentration on one or two clients, niche specialisation outside the buyer's wheelhouse, or unresolved professional issues. Some of these are uninsurable for buyers without significant terms protection.

- 1.0x to 1.3x GRF. Most decent general-practice books. Recurring revenue 60 per cent or higher, healthy client mix (no client over 15 per cent), clean PII history, sensible client retention going into the deal. The band most realistic deals close in.

- 1.3x to 1.5x GRF. Premium books. Recurring revenue at 75 per cent or above, strong client mix, sector specialisation that fits us (tax-led, niche advisory, HNW personal tax, owner-managed business specialism), clean track record. We will pay 1.5x GRF for the right firm.

So the band we quote in a serious conversation is 0.9x to 1.5x. The specific number falls out of the eight factors covered in our GRF multiples explainer. A £500k book with 80 per cent recurring revenue and a clean client mix typically lands at 1.1x to 1.3x in our pricing. A £750k book with strong recurring revenue and a sector specialisation that genuinely fits us can reach 1.4x to 1.5x.

EBITDA multiples: where these apply

For practices over £750k turnover with proper management accounts, the conversation often shifts from GRF multiples to EBITDA multiples. The realistic range:

- 4x to 5x EBITDA. Most regional buyer-side pricing for chartered firms in our size range.

- 5x to 6x EBITDA. Larger regional buyers and the smaller PE platforms. We can get to this range for the right book.

- 6x to 8x EBITDA. The larger PE platforms, for books that fit their thesis (typically over £1m turnover, with growth potential, in a target geography).

If your practice is over £750k and you have clean management accounts, we will run both calculations on the GRF basis and the EBITDA basis. We then quote against the more favourable of the two for the right book. The seller should not be penalised by the calculation choice.

Worked examples at three GRF levels

The following are illustrative worked examples, marked as such. They are not prior-deal disclosures.

Example A: £250k GRF, 75 per cent recurring

- Estimated headline value: £225k to £300k (0.9x to 1.2x)

- Mid-point quote: £262.5k

- Cash on completion: £131.25k

- Month 12: £65.625k

- Month 24: £65.625k, subject to retention test

- Total over 24 months: £262.5k, assuming retention at or above 85 per cent

Tax structuring (see disclaimer below). The typical route is an asset sale via the existing limited company. Proceeds are taxed at corporation tax rates and then distributed to shareholders. Business Asset Disposal Relief considerations depend on the shareholder profile. Pension contributions out of pre-completion profits at corporation-tax-deductible rates can be an attractive route to convert taxable income into pension wealth before sale. The two-tax-year window before completion is the standard planning horizon.

Example B: £500k GRF, 80 per cent recurring

- Estimated headline value: £550k to £650k (1.1x to 1.3x)

- Mid-point quote: £600k

- Cash on completion: £300k

- Month 12: £150k

- Month 24: £150k, subject to retention test

- Total over 24 months: £600k, assuming retention at or above 85 per cent

Tax structuring at this scale. Share sale becomes a viable alternative to asset sale, with different consequences for the seller's tax position. Share sale typically taxes the seller at 18 per cent under BADR up to the lifetime limit (rate from 6 April 2026, subject to the seller meeting the qualifying conditions). Asset sale, by contrast, taxes corporate proceeds at corporation tax rates plus shareholder distribution. The choice depends on the buyer's preference, the seller's circumstances, and the structure of the seller's holding. Independent tax advice is essential; the questions to take to your independent tax adviser are set out separately.

Example C: £750k GRF, 85 per cent recurring, sector fit

- Estimated headline value: £900k to £1.125m (1.2x to 1.5x for a premium book that fits us strategically)

- EBITDA crosscheck: at typical 35 per cent EBITDA margin, EBITDA is £262.5k. 4.5x to 5.5x EBITDA gives £1.18m to £1.44m. We use the higher of the two methods to ensure the seller is not penalised by the calculation choice.

- Mid-point quote on a strong fit: £1.0m

- Cash on completion: £500k

- Month 12: £250k

- Month 24: £250k, subject to retention test

- Total over 24 months: £1.0m, assuming retention at or above 85 per cent

At this scale, comparison with PE platform offers becomes meaningful. A £750k book with healthy EBITDA margins might attract 5x to 7x EBITDA from a platform. That is £1.3m to £1.84m headline, with the trade-offs described at the top of this page. The decision is a function of seller priorities. We will quote against the platform for the right firm. The seller chooses based on net-to-pocket and structural cleanliness, not headline alone.

To run these numbers for your specific book, send five data points through our indicative valuation page or book a 15-minute confidential call. Mutual NDA on request before any substantive conversation.

How we fund the deal

A seller will reasonably ask whether the buyer can fund the completion payment and the two deferred tranches. The answer matters more than most marketing pages on this subject acknowledge.

Completion payments come from Jack Ross's own balance sheet. The funds do not come from a brokered buyer pool, a syndicate, or a deal-by-deal external loan. The firm holds working capital and reserves sufficient to fund the deals it agrees to do. Where a particular transaction needs an external legal or banking process (rare at our deal sizes), we say so at heads of terms, before any exclusivity becomes meaningful. We do not ask a seller to stop other conversations without first showing that the structure is fundable.

Tax structuring: asset sale versus share sale

The choice has material tax consequences. The summary, with the strong caveat that individual circumstances determine the right answer:

Asset sale. The buyer (us) acquires the goodwill, work in progress, fixed assets, and (usually) employment contracts of the practice. The seller's company retains its corporate identity, settles outstanding obligations, and distributes the proceeds to shareholders over time. Corporation tax applies on the gain at the company level. Subsequent distribution to shareholders is taxed as dividend income or as capital on liquidation, depending on structure. The buyer typically prefers asset sale because they pick and choose what they take.

Share sale. The buyer acquires the shares of the company that owns the practice. The seller's company changes ownership. The assets, liabilities, and contracts inside the company all transfer with it. The shareholder is taxed on the capital gain at CGT rates (18 per cent under Business Asset Disposal Relief up to the lifetime limit, 24 per cent above; rates from 6 April 2026 and subject to change). The seller usually prefers share sale because of the BADR-protected single capital gain treatment.

The negotiated structure is often a compromise. Most of our deals are asset sales but with specific accommodations on liability allocation that approach the seller-friendliness of a share sale.

Pension contributions before sale. A genuine planning opportunity for sellers in their late 50s and early 60s. Personal pension contributions made by the company on behalf of the working principal in the two tax years immediately before sale are deductible against corporation tax (subject to annual and lifetime allowances). They convert taxable corporate profits into tax-protected pension wealth. The numbers are material. A principal earning £180k a year as the working partner of a £500k-fee practice may be able to contribute £60k to £80k a year for two years. That shifts around £120k to £160k of value into the pension wrapper at 100 per cent corporation tax efficiency. The annual allowance, taper rules, lifetime allowance, and recent budget changes affect the available headroom; this needs specific advice.

Standard caveat (this matters). The tax structuring described above is general guidance and depends entirely on your individual circumstances. The right answer depends on the structure of your firm, your other income, your pension position, and the specific terms of the deal. We recommend you take independent tax advice, ideally from a tax specialist who has not been involved in the firm's day-to-day work. The advice should be paid for separately from any deal contingency. We will work co-operatively with whichever adviser you appoint.

What the structure protects against

This structure exists because the longer tail is where deals go wrong. Specifically:

- Buyer financial difficulty in years 3 to 5. Multi-year earn-outs make the seller an unsecured creditor of the buyer for years. PE platforms have refinanced, restructured, and (in one or two cases) entered formal insolvency processes within the typical earn-out window. Our 24-month structure means most of your money is in your hands long before any of those scenarios become live.

- Deferred consideration disputes. The longer the earn-out, the more conditions and metrics are involved, and the more room for disagreement on whether they have been met. Our structure has one retention test, against one defined number, at one point in time.

- Continuing seller involvement creating disputes. Earn-outs that require the seller to remain involved create perverse incentives on both sides. Our structure does not require any continuing involvement after the 12-week handover.

Questions you will want to ask us

The GRF multiple is calculated against the GRF at completion, not at heads of terms. If your book grows during the 12-week run-up, the deal value goes up correspondingly. Growth could come from new clients you would have signed anyway, or from annual fee increases landing. If your book shrinks, vice versa. The mechanism is symmetric and written into the heads of terms.

Material adverse change clauses cover this. If a client representing more than 5 per cent of the book leaves before completion, both sides have the right to renegotiate or walk. Walking-away costs are limited to professional fees actually incurred up to that point.

Specifically: gross recurring fees from the original acquired client base at month 24, divided by gross recurring fees from the original acquired client base at completion, must be at least 85 per cent. Adjustments are made in three cases. First, clients lost through death or business closure unrelated to the deal. Second, clients off-boarded by mutual agreement at the time of the deal. Third, any client where the acquired-firm seller has subsequently taken on a continuing professional role with that client. New clients we win post-completion are not included in the calculation.

One Heads of Terms (typically 3 to 5 pages). One mutual NDA (1 page, signed at the start of substantive conversations). One Sale and Purchase Agreement (typically 30 to 50 pages). One disclosure letter. One transitional services agreement covering the 12-week handover. Your solicitor reviews all of it. Our solicitor reviews all of it. The negotiation typically runs to two to three rounds of mark-ups.

We are a tax practice and we will discuss the structure with you in detail. We do not provide formal tax advice on which you would rely; that needs to come from an independent adviser engaged separately. Our willingness to discuss is upside, not advice.

The next step

If the structure makes sense as a starting point, the right next step is a 15-minute call. On that call we can run the numbers for your specific book and give you an indicative range. No commitment, and no NDA is required for the first call. If you would prefer a mutual NDA in place before the call itself, ask in your first email and a one-page mutual NDA comes back signed-ready within the hour.

Related reading

- Get an indicative valuation range - interactive calculator, five data points, instant defensible range with the 50/25/25 cashflow.

- GRF multiples explained - the eight factors that move a UK accountancy practice between 0.7x and 1.4x GRF.

- The 12-week timeline - how the structure plays out across the deal sequence.

- Private equity vs trade buyer - present-value comparison of the two routes.

- Selling your accountancy practice: the practical guide - the overview of all available exit routes, with the seller economics on each.