Twelve weeks. A clean exit. A defined finish line.

Why the timeline matters

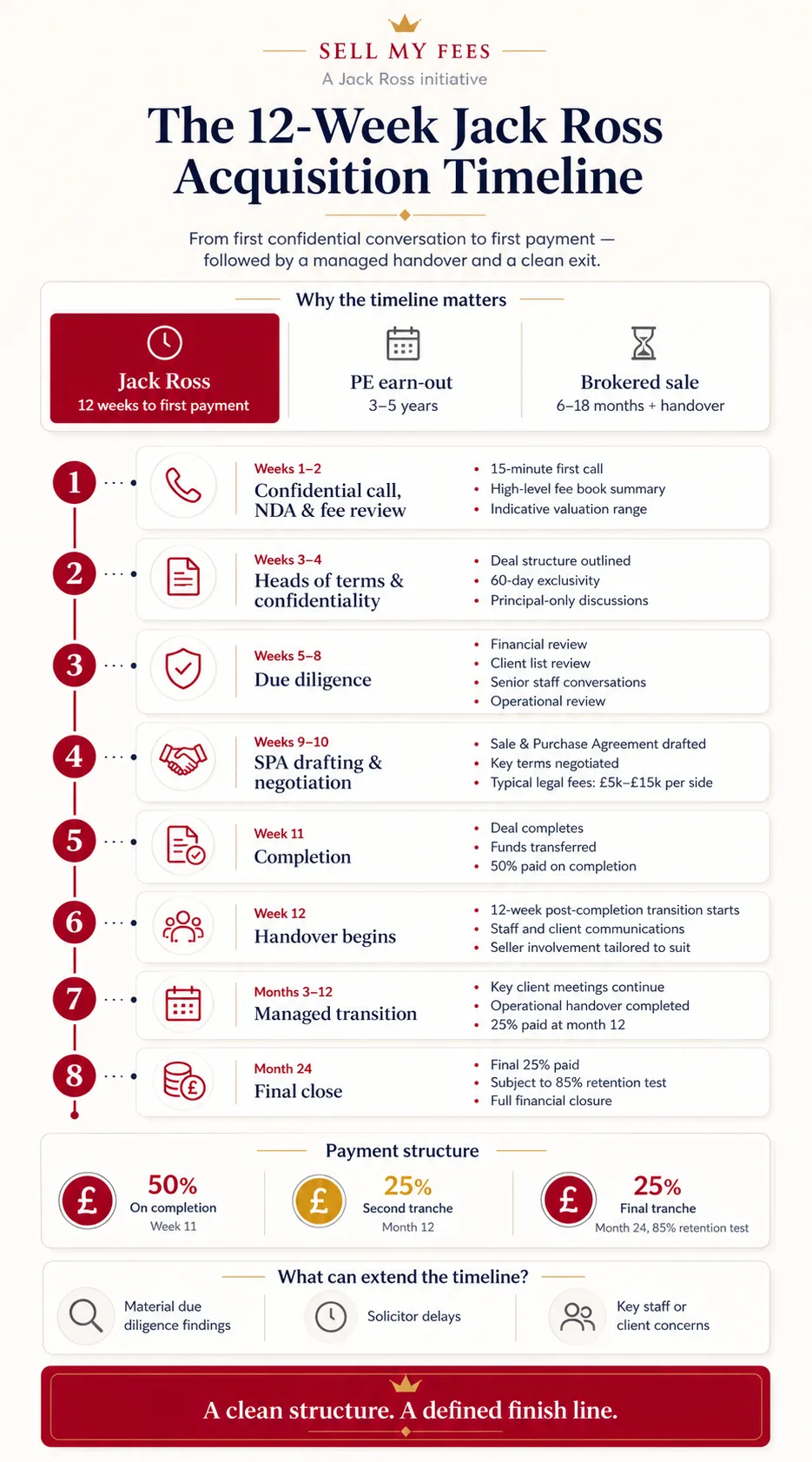

The two alternative routes to exit operate on much longer clocks. PE consolidator earn-outs typically lock you in for three to five years after completion. Broker introductions can take six to eighteen months from listing to completion, and another three to six months of handover after that. In the wider UK accountancy M&A market, neither route returns full value to the seller inside a year.

For a principal in their early sixties, the difference between a 12-week structure and a 5-year structure is the difference between a defined retirement date and an open-ended drift. The numbers come out broadly comparable in many cases. The clock does not.

The twelve-week transition (sometimes called integration in the consolidator playbook) is the same operational process under either label. We use the word transition because it describes what happens for the seller. Integration describes the same sequence from the buyer's side of the table.

The 12-week sequence

Weeks 1 to 2: NDA, initial conversation, fee book review

The first conversation is 15 minutes. It can be by phone or video, whichever you prefer. We do not need any documents to have it. We will tell you, on that call, whether your practice fits our acquisition profile and whether the conversation is worth continuing.

If both sides want to proceed, the second meeting is 60 to 90 minutes, in person if you are within reasonable driving distance of Manchester, or by video. Before that meeting we sign a mutual NDA (a one-page document sent on request). You share a high-level fee book summary: total fees, recurring proportion, top-ten client concentration, year-on-year fee history, staff numbers and pay grades. We review and come back with an indicative valuation range and any clarifying questions.

End of week 2: you have an indicative range and you know whether we are serious.

Weeks 3 to 4: heads of terms, confidentiality protocol

If the indicative range works for you, we draft Heads of Terms. The document is typically 3 to 5 pages. It covers: deal structure (50/25/25), indicative price (range, narrowed by completion of due diligence), key conditions, exclusivity period (60 days), and the handover principles for staff and clients. Your solicitor reviews. We address any reasonable change. Heads of Terms are signed.

Confidentiality protocol kicks in. Your team have not been told anything yet at this point, by design. Conversations are between principals only. The list of who knows on each side is logged. We use code names for the deal in any written correspondence until completion.

Weeks 5 to 8: due diligence, client list review, staff conversations

This is the substance of the deal. Due diligence runs in parallel across four workstreams. The process is intensive but contained inside this four-week block, by design; it does not drift into months six through nine, as it does on broker-led deals.

Financial due diligence. Last three years' management accounts, statutory accounts, debtors and WIP, recurring versus non-recurring split, fee schedule, client concentration analysis. We run this internally; no external accountant fees on our side. Your solicitor and our solicitor co-ordinate the data exchange under the NDA.

Client list review. Anonymised client list with annual fees, services, year acquired, and contact tier. We work through the list together to identify the top 20 per cent of the client base for joint introduction meetings, any clients with current or recent disputes, any clients you are concerned about for the transition.

Staff conversations. Your senior staff are told in week 5 or 6, after Heads of Terms is signed and before the SPA is drafted. We attend the conversations with you if you would like, or we attend separately. Junior staff are told in week 9 or 10, closer to completion. We provide template communications, tailored to your specific firm, that you and we co-author.

Operational due diligence. Lease, supplier contracts, software licences, PII, professional registrations, ICAEW practice review history, complaints history. We work through the lot.

Weeks 9 to 10: SPA drafting and negotiation

The Sale and Purchase Agreement is drafted by our solicitor and reviewed by yours. Typical document length is 30 to 50 pages. The substantive negotiations are usually limited to: warranty schedules (what you warrant about the state of the practice), indemnity caps (how much exposure you retain), the precise wording of the retention test for the month-24 payment, the transitional services agreement covering the 12-week post-completion handover, and any specific staff or client commitments that need to be in the deal document rather than in side correspondence.

Most deals settle after two rounds of mark-up. Some go to three. The cost of solicitor fees on each side is typically £5k to £15k depending on complexity; this is built into your budget for the deal, not something that comes out of the headline price. Independent legal advice on your side is essential; we expect you to take it and we work co-operatively with the adviser you appoint.

Week 11: completion, payment 1 of 3

Completion is a fixed date, agreed at signing. Funds clear into your nominated account on completion day or the working day after. Disclosure letter is signed. Warranties are given. The deal is done.

Week 12: handover begins

Week 12 is the start of the 12-week handover, which runs from completion through into months 2 and 3 post-completion. Staff communications go out to your full team in week 12 if not earlier. Client communications go out by post for clients over 65 and by email for everyone else, signed by you and our Managing Partner jointly.

You are present in the office, full or part time as you prefer, through the first 12 weeks post-completion. Your level of involvement is your call. Most retiring principals come in three days a week for the first month and reduce to one day a week by month three.

If the timeline maps to your situation, the first conversation is a 15-minute confidential call. Book a call. Mutual NDA on request.

Months 3 to 12: managed transition

By month three, your formal involvement reduces to one day a week or less, by mutual agreement. Joint client meetings continue for the top 20 per cent of the client base across months one to four, on a calendar agreed at completion. Software handover, supplier transitions, lease decisions, and any office-relocation work all complete in the first six months. This is the period in which most of the operational integration work lands.

The Transitional Services Agreement signed at completion sets out the structure of your involvement and the corresponding fee paid to you (typically a modest day rate to cover your time, separate from the deal consideration). It is enforceable in both directions: you commit to availability for an agreed number of days; we commit to use that time appropriately rather than asking for help on every routine matter.

By month 12, formal involvement is complete. You are available on call for any genuinely seller-specific question (a client phoning to ask about a 1995 conversation, a historic file query, a tax position you set up that needs explaining). Most months bring one or two calls. Some months bring none.

Month 13 onwards: you are gone

Month 13 is the first month with no formal commitment. You are retired, on whatever timetable that means for you. The second tranche payment lands at month 12 (the prior month).

Operationally gone, not financially gone. Worth being clear about this. Your final 25 per cent remains subject to the retention test until month 24, and the formal SPA warranties continue running on their normal indemnity periods. The phrase "gone" describes operational involvement, not financial closure. The deal is fully closed at month 24 once the final tranche pays.

If you are interested, we keep in touch informally. Some former principals stay in occasional contact. Some we never see again, which is also fine.

What the seller does during each phase

The 12-week sequence above describes what the deal looks like from outside. What it asks of the seller, week by week, is a different question and one most retiring principals want answered specifically before agreeing to start.

Weeks 1 to 2: fee book extraction. The seller's task is to produce a single summary spreadsheet showing total fees by client, recurring versus non-recurring split, year acquired, primary service, and a tier indicator (top 20 per cent, middle, tail). Most practice management systems export this directly. The work takes a competent practice manager half a day; the principal reviews and anonymises before sending. Nothing else is required in the first fortnight.

Weeks 3 to 4: solicitor briefing. The seller appoints a solicitor with prior experience of small-firm sales (not all corporate solicitors have this; ask for two reference deals before instructing). Brief on the indicative range, the proposed structure, and the timeline. Hand over the heads of terms when issued. Solicitor reviews and proposes any changes; the principal-to-principal call resolves the substantive points before the lawyers redraft. The seller's time commitment is two to three hours.

Weeks 5 to 8: due diligence cooperation. The bulk of the seller's work falls here. The buyer issues a due diligence request list (typically 40 to 60 line items covering financial, operational, regulatory, and HR matters). Most items are documents the practice already holds and can be uploaded to a secure data room within a day or two. Items requiring narrative explanation (the history of a particular client relationship, the rationale for a specific accounting treatment, the background to a past complaint) take the principal's direct attention, typically four to six hours across the four weeks. The senior-staff conversation in week 5 or 6 is the most emotionally substantive task in the whole sequence; allow a full half day for it and treat it as a single block, not a corridor conversation.

Weeks 9 to 10: SPA review. The seller's solicitor leads on document review. The principal's role is to read the warranty schedule personally, query anything the seller would not be able to warrant in good faith, and instruct the solicitor to negotiate the qualifications. The disclosure letter is the seller's own document and must be drafted personally with solicitor support; it is the seller's primary protection against post-completion warranty claims, and an under-drafted disclosure letter is the single most common cause of avoidable disputes. Budget six to eight hours of focused work in week 9.

Week 11 to week 12: client letter drafting and software access. The seller drafts the client communication in week 11, working from a template, signed jointly with the buyer for week 12 release. Software credentials, bank mandates, payroll administrator changes, and supplier handovers are scheduled for the working week immediately after completion. The seller's calendar for week 12 should be cleared of routine client work; it will be needed for the handover meetings.

What can go wrong, and how we mitigate

The 12-week sequence assumes a deal that proceeds without interruption. The realistic scenarios that extend it:

- Material due diligence finding. Something we did not know at heads-of-terms stage emerges in week 6 or 7. Common examples: a client with an undisclosed retention concern, a staff member with a grievance not previously raised, a tax position that needs restating, an ICAEW practice review issue not resolved. The deal does not necessarily fall through, but the timeline extends by 2 to 4 weeks while it is worked through.

- Solicitor delays. Either side. The mark-up rounds take longer than planned. Usually adds 1 to 2 weeks.

- Staff or client objection. Rare but happens. A senior staff member declines to come across; a top-five client signals they will leave; in either case the deal economics need to be reviewed and the heads of terms re-signed.

- Seller cold feet. Also rare and also legitimate. If at any point during the 12 weeks the seller has serious second thoughts, the right answer is to pause the deal and reconsider. We commit to that without prejudice: if you decide at week 8 that the timing is wrong, we close the conversation and absorb our own professional costs without pursuing the matter. The conversation can resume later if the timing changes.

The structure is reversible up to completion. After completion, the only seller-side reversal mechanism is the retention test against the final 25 per cent, which is symmetric and written into the SPA. The value of the deal to both sides is preserved by the test mechanic, not by litigation routes.

Questions you will want to ask us

Sometimes. If your book is straightforward, your accounts are clean, your solicitor is fast, and there are no client or staff complications, the sequence can be run in 9 weeks. We do not recommend trying to compress it under 9 weeks; the substantive due diligence cannot be done faster than that without taking on risk that comes back to bite both sides.

Yes, if there is a reason. Some sellers want to time completion to a tax-year boundary, or to wait until a major client has renewed for the year, or to give themselves time to wind down a personal commitment. We accommodate within reason. The structure was designed to be 12 weeks because the practical execution falls into 12 weeks naturally and longer creates new problems (staff anxiety, client speculation, momentum loss), not because we are in a hurry.

By default, formal involvement ends at month three post-completion. The Transitional Services Agreement covers months one through twelve at a flat day-rate plus the deal consideration. From month 13, there is no formal arrangement. You are available informally for genuinely seller-specific queries; we are available informally to you for any continuing personal accounting work you might want.

For most sellers, completion either side of 5 April is broadly tax-neutral on the deal proceeds (the gain crystallises on completion regardless), but timing can interact with personal tax planning, pension contributions, and the seller's own income position. If tax-year timing matters to you, raise it at heads of terms and we calendar accordingly. Independent tax advice on the timing question is sensible.

The next step

If the timeline works for you, the right next step is the 15-minute first call. We can talk through your specific situation, identify any timeline-affecting factors, and give you a more precise calendar. If you would prefer a mutual NDA in place before the call, ask in your first email and a one-page mutual NDA comes back signed-ready within the hour.

Related reading

- Your staff are not a redundancy line item to us - what happens at week 5 to 6 when senior staff are first told.

- Your clients should barely notice the difference - what happens in months 1 to 4 with joint client meetings.

- A clean structure, not a leveraged earn-out - payment landing dates correspond to weeks 11, month 12, and month 24.